Apple’s weapon of choice

THAT'S a phone?

It was interesting that when Phil Schiller decided to start taking pot shots at Android he lighted on the same old argument.Fragmentation

“We are hearing this week that the Samsung Galaxy S4 is being rumored to ship with an OS that is nearly a year old” he said (turned out that actually he was wrong – although the competing HTC One will be shipping on 4.1).

My suspicion, though, is that Samsung will be having the last laugh. While the Galaxy S IV is a pretty ugly, utilitarian chunk of plastic. Dieter Rams would, no doubt, be turning in his grave. But backed by a marketing budget the size of Wales, I would put good money on it being the bestselling phone this year full stop. If the 2013 iPhone is just a 5S, I think Apple’s market share is in for another spanking.

|

| (With apologies to Crocodile Dundee) |

Why fragmentation will (supposedly) kill Android

The bear case on Android fragmentation is one we've heard again and again. At its heart its very simple:

- Android’s open hardware ecosystem and customisable source code would lead to fragmentation into an an unsupportable mishmash of OS versions, hardware vendors and screen sizes.

- As Android sold all its units into mid/low end users spent far less money on Android than on iOS.

- Faced with unaffordable app complexity and low revenue customers, developers would be unwilling / unable to build Android apps.

Except it hasn't quite happened like that:

And as Google Play store approaches the million-app mark, it starts to overtake the iTunes App Store in terms of size (yes I know appstore quantity is no guide to quality… but you get the point).

In short: The fragmentation threat has been consistently overstated by commentators and analysts. It hasn't held back Android growth. It hasn’t stopped big-name apps from being available on Google Play. And, in my experience, it hasn’t really affected the end user.

Three myths about Android fragmentation

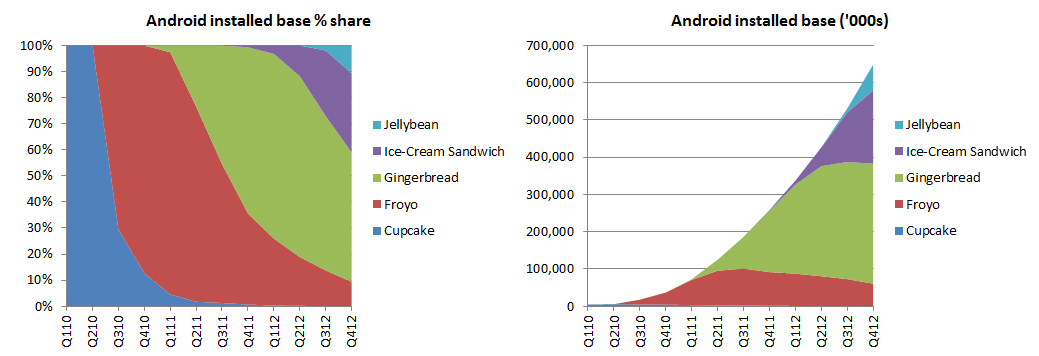

Myth 1 - The Android base is hopelessly fragmented

- Remember the law of large numbers: The chart above left shows how Android version fragmentation is most frequently presented. It looks pretty bleak. Slow adoption of each successive Android version keeps the base in a state of continual fragmentation. BUT, if you rebase it in absolute terms (chart above right) the picture is actually far less bleak. Six months in, Android 4.1 may still only be 10% of the market, but that represents 60m devices. In contrast at this stage in its cycle Android 2.0/2.1 30% market share… but that was only 4m devices. Remember - it isn’t the relative fragmentation which drives app developer economics – it’s the absolute size of the addressable market. While this market might not be as big as the iOS market (yet), its certainly more than worth the effort.

- As the platform matures, change (and fragmentation) slows: Also as Android matures the differences between different versions become less and less. While the UI skin changes and services get added on, the rate of fundamental change starts to slow down, lessening the burdens for developers. It’s interesting to note that people tend to lump ICS and Jelly Bean together when they talk about the Android installed base. It’s not just version number semantics – 4.2 was definitely more of an evolutionary change.

Myth 2 - Developing on Android is an insurmountable technical challenge

Actually this is partially correct. Because you have to test against a number of different devices, Android is harder to develop for – even big mobile houses like as Gameloft will admit this. It’s no surprise that cool new apps such as Recce or Flipperdiet (a cute attempt by an ex- competitor of mine to gamify your snacking urges) come out first on iOS and often stay on iOS. Particularly given that iOS users spend so much more on apps per head. However once you start to get to larger scale apps that logic starts to fall apart:- The Android burden becomes a hygiene factor for bigger devs: If you look at the top-ten lists on the iTunes and Google app stores they are dominated by the same old names. Zyngha, Gameloft, EA, Rovio et al. For these guys the hassle of developing Android isn’t really a barrier – given their resources its more of a hygiene factor. And it actually becomes a competitive advantage to develop on Android given smaller startup competitors will struggle to get their apps to work on the platform.

- Better tools help: As the Android development market matures we are also seeing increasingly better software tools. Cross-platform development tools will only get better, and more importantly we are seeing increasingly sophisticated testing tools to address the device compatibility issue. For example Keynote’s Deviceanywhere package gives you a virtual sandbox which allows you to test against virtual devices – its not as if you literally need to have dozens of handset lying around your office to do your testing.

- Samsung and Mediatek provide consistent platforms: As the Android market matures it is consolidating. This also helps fragmentation. At the high end the rise of Samsung means that its Galaxy phones are the dominant platform – ensure compatibility with Samsung’s top half-dozen platforms and you will have the vast majority of the wallet-share sewn up. At the low-end Mediatek solutions are powering hundreds of low end (and sometimes less low-end devices. Again while technically there is massive device proliferation – actually the guts of these will be increasingly similar and easier to test against.

- Screen size frag is overrated: Also note that concerns around screen size fragmentation have always been overblown. From the start Android has pushed developers towards resolution-independent scaling. I’ve used Android devices with screen sizes of 2.5”, 3.0”, 3.7” and 4.0” and you know what? Temple Run scales nicely across all of them. (Side note: iOS has also always had similar capabilities, but as iOS screen sizes much less fragmented the functionality was much less used by devs. I suspect this has been one of the factors holding them back from moving to larger portrait form-factors; the iPhone 5’s stretched widescreen on the iPhone 5 feels like a kludge designed to ensure backward compatibility with a non-scalable legacy apps base.)

- The move to webapps gets around many of these issues: I’m not going to labour this point – HTML5 webapps have so far flattered to deceive. But if webapps (or websites repackaged as apps) do ever up their game this circumvents much of the burden of native app development.

Myth 3 - There is no money in the Android ecosystem

Again there is a lot of truth to this argument. Spending per user for Android remains stubbornly low. Can’t be much money to be made there.However if you believe that then I think you are wrong:

- The economics change for larger developers: Once you get to scale the arithmetic around Android users spending is less of a barrier. Remember the economics become different as you scale on a fixed cost base. Remember if you are a start-up developer then whether you’re 100 paying customers give you ten bucks or one buck matters. If you have a 100,000 users and you’ve covered your fixed cost base, then an additional Android users is equally as profitable as an additional iOS user; sure on a per-user basis they’re not as profitable but the marginal profitability is the same. Sure if the sales & marketing spend on Android and iOS users is segmented this would impact profitability, but my suspicion is at the mass-market level the S&M overhead blurs into one.

- The rise of freemium changes the game: Closely related to the large dev issue is the rise of the freemium model for apps, particularly games (most notably the recent Real Racing 3). Remember the freemium model works by blooting out the largest possible install base, and relying on a very small proportion of them to convert to paying customers. If its customer volume’s you are chasing, then the Android market is one you cannot ignore. Remember, in the freemium world every penny counts…

- Barbell economics: For a start, mix ignores the profitable (and growing) high-end segment). Yes the average spend per Android user is low – this is due largely to the mix being skewed towards he low-end and emerging markets. However the success (and dare I say it, increasing dominance) of the Galaxy S devices means that there is also a significant – and growing – high end installed base who have just as much disposable income as an iPhone user. In short I suspect the Android installed base looks like a barbell in economic terms – on average the average spend looks bad but there’s actually a lot of wallet-share to go for in the top-20% (which are largely concentrated on a small number of devices – viz consolidation/testing point above).

- Profitability is a backward-looking indicator: The big-walleted iPhone/small walleted Android argument is also making an implicit point: That we should assess the future prospects of an ecosystem via its profitability (iOS 70% profit share good: Android (or shall we say Samsung) 30% profit share bad). In reality, profitability gives a good view of the current situation in the market but is a terrible guide to its future profitability. After all Nokia remained the dominant player by profit share for years after its decline was apparent.

{kind=link}

|

| Vertu's Android launch shows iPhone users aren't the only people with more money than sense... |

To conclude, I’m not saying fragmentation doesn’t exist. And I’m not denying it’s a PITA for all those app devs out there. What I am saying is that, contrary to what the commentariat think, it hasn’t held back Android in the past, and I doubt it will in the future.

Postscript: Two (better) arguments why fragmentation will remain an issue

As I hope I’ve shown, the empirical evidence shows the fragmentation problem has been significantly overstated, and the situation is only likely to improve. Does this mean we stop talking about fragmentation? I suspect not, and think there are two (better) reasons why fragmentation will remain on people’s minds, even if it isn’t the killer issue:Fragmentation is a weapon Google can use against Android forks

The biggest threat to the survival of Android isn’t actually iOS. Its Android itself. As vendors such as Amazon, Baidu (or maybe one day Samsung…) fork the OS, they can take advantage of the massive app ecosystem, but cut out Google’s online services (and ad dollars). One obvious tool to combat this is by adding new features to Android which break backward compatibility with older forked versions. This doesn’t kill the competition, but it slows it down (e.g. the Kindle Fire tends to be based on a version of Android which is roughly a year old).Fragmentation means security holes remain unpatched

The biggest issue with fragmentation isn’t actually app compatibility, it’s system security. Outside of Google’s flagship Nexus devices, system updates tend to be relatively slow in coming which means critical security vulnerabilities remain unpatched. As more and more personal data is loaded onto mobile devices this is an increasing weakness versus iOS, where Apple can roll out patches across the majority of the installed base relatively quickly. Stuxnet for legacy Android devices anyone?