Last month’s most significant phone launch was...

The Galaxy SIV has landed.

So with this year’s Galaxy SIV being bigger, brasher and badder in every respect, you’d expect this to be April’s most significant phone launch.

But I would disagree.

I think the most significant phone launched in April wasn’t the identikit SIV (or even the gorgeous, aluminium-tastic HTC One).

It’s a Nokia.

Half-price heroes

The Nokia Lumia 520 is a beautiful little device. Its sculpted matte back has a slight cast-iron finish which harks back to the N9’s classic unibody. Its 4” screen is the goldilocks size for everyday use (not to big, not too small). Its tapered edges mean the xxmm thickness feels svelte in the hand. It feels like a damn sight classier than the shiny, plasticky Galaxy SIV.

But there’s the rub. Because this is a phone that costs £109 no-strings-attached (£99 on O2 PAYG + £10 top-up; NB apart from iPhones, Carphonewarehouse devices are usually carrier-unlocked). That's an astonishing price for a brand-new, dual-core, carrier-unlocked smartphone.

While the mighty SIV is most definitely more of the same (Samsung has clearly gotten so bored of copycatting Apple that it has started copycatting itself!), the Lumia is a device that takes Windows Phone to entirely new price points.

It’s what I call a “Half-Price Hero”.

|

| The legendary San Francisco |

These are the half-price heroes – low cost smartphones which give back twice what you pay for them.

How do handset vendors make money from these products? Well the answer is they don’t – they are usually “strategic” products sold at low or low margins to gain share. In effect the vendor is paying you to use their product – and you’re getting a smartphone you’d have gone and bought anyway into the bargain. The Blade was a result of ZTE’s desperation to get a foothold in the smartphone market. The Nexus 4 was Google’s attempt to subsidise its way into a leading smartphone position.

The Lumia 520 is the result of a similar dilemma. Nokia - facing smartphone extinction – has basically decided to trade gross margin for market share. Not a sustainable strategy I’d give you, but one which suits Joe Public to a tee.

Thankfully they’ve also picked a cracking device to do it with.

The Lumia 520: Thoroughly Reviewed

Design

|

The cast-finish is a nice touch. It scrubs up well vs. the

cheap glossy plastic on the Android competition...

|

And thank heaven they’ve opted for a matte finish. Rather than a glossy fingerprint magnet you get a slightly rough surface which feels like gently cast iron. It actually looks good when smudged with oily hands. Colour-wise it’s available in what are fast becoming Nokia’s signature shares – cyan, red, yellow and white (as well as black). At this price point it’s a good a chunk of

Display

|

| Screen: Good enough. |

A final bonus – the display is one of the new-fangled ultra-sensitive ones (cf Galaxy SIV) which works when with gloves. Limited usefulness in target markets such as India, but at least it gets round Nokia’s “how do we use a phone in -20c Finnish winters” problem (which I suspect was one reason why they stuck with horrible resistive touch screens for so long - N900 I’m looking at you!).

Internals

The guts of the phone are where it really shines. You basically get the exact same platform as the more expensive 620, 720 or HTC 8S – a dual core Snapdragon (albeit at slightly lower clocks). That’s one advantage of bargain-basement shopping on Windows – vendors aren’t allowed to cut back on the internals due to Window’s rigid hardware requirements. There’s also a microSD slot (works nicely with my SanDisk 64GB microSD) and a removable battery.NB Initially the device didn't recognise the 64GB (or any) microSD out of the box - although it did after a quick factory reset. New users please bear this in mind!

|

The Lumia 520 and the iconic N9: The difference is that one

phone launches at 20% the price of the other one...

|

Now the bad news – like most low-end WP8 devices the 520 only has 512MB of RAM. This isn’t a disaster – in day-to-day use the phone is just as snappy as 1GB devices. However a few of the higher end games (Temple Run, Modern Combat 4) require 1GB to run. Not a deal-breaker but it means the phone is less future-proof than 1GB models.

Two more omissions: No NFC (the chocolate teapot of the wireless technology world) and no LTE. Then again for £109 you can always bin it and buy another phone when that finally starts to matter…

Battery life, camera

Battery life has always been a key issue for me – if you’re on the road for business you can't have your smartphone die on you after lunch. Thankfully the Lumia 520 has a removable battery for us road-warriors which clocks in at 1430 mAH. Interestingly that's 10% bigger than the battery on the higher-end Lumia 620 (same internals but a smaller screen). Anyhow the bottom line is that the battery life is adequate – it will get you through a day and is pretty durable on standby, although the phone’s no RAZR MAXX HD.

The camera is a 5MP shooter; Nokia economise by including no flash.. It does the job – pics are sharper than on my previous Android device. Can’t ask for more at the price.

|

Camera (raw photos): Perfectly adequate for close-ups and long-shots.

(FYI The pork buns are the Momofuku rip-offs from from Yum Bum near London's Old Street)

|

Oh and before you ask it makes phone calls perfectly well. Not that people use phones to make phonecalls anymore!

Software

|

The Metro home screen and the WP8 Ecosystem:

More than good enough.

|

And after a month of using it as my daily driver I can honestly say that Windows Phone feels feature-complete. What really stands out is the deep integration of online services like Twitter, Facebook and Linkedin natively into the OS (nb how Facebook Home apes this). That’s one area where the silo-ed iOS still feels some way behind. For both Windows 8 and WP8 Microsoft have done a great job integrating online services into the fabric of their OS, a stark contrast to both OSX and iOS. Google finally have serious competition in providing online services.

The one bugbear is multi-tasking. Apps often have to restart when you switch back into them rather than just picking up. There’s a small pause here while it reloads (not as big a deal as people make out actually), but it means you might lose what you were doing at the time (mainly games or media playback). On the positive side the ruthless app-killing means that even with 512MB RAM there’s never a lag when you have lots of apps loaded up (or not loaded up as it seems) – a perennial problem with low-end Android.

Much has been made about Google’s attempts to make it harder to integrate its Calendar/Email services. I take this as a back-handed complement – the fact that Google is going after Microsoft’s online services much more aggressively than it has done against iOS is an acknowledgement of how good they are getting as competitive offering. But in practice I had little problem setting up my Gmail and multiple calendars. I suspect this is a situation which will only get easier.

App ecosystem: The two big challenges

Obviously the app ecosystem lags iOS and Android, but unlike many commentators I think the Windows Phone 8 ecosystem is now good enough. That might be a controversial judgement for some, so let me flesh this out.I think there are two big challenges for any non-iOS/Android ecosystem. The first is cutting edge apps which tend to come up on iOS first – things like Summly or Mailbox which are incredibly cool and innovative. These apps will remain with iOS for the foreseeable future. But do bear in mind, these apps are often too bleeding edge for everyday use; IMHO Summly was more a tech demo than a service.

The second challenge area is when you have one crucial app you can’t live without (think Spotify, Hulu). That is the biggest weakness of the WP8 ecosystem, but I would say though that support for big-name apps is decent and improving. Marquee programs like Evernote, Spotify, Bloomberg or Linkedin are all available. Also Microsoft and Nokia have a good range of own-label offerings to help fill the gaps. Microsoft is been particularly good at pushing high-end gaming offerings – from the incredibly cute mobile Office and MSFT’s game offerings to a bunch of Nokia exclusives like Here maps, Photobeamer and Mix Radio.

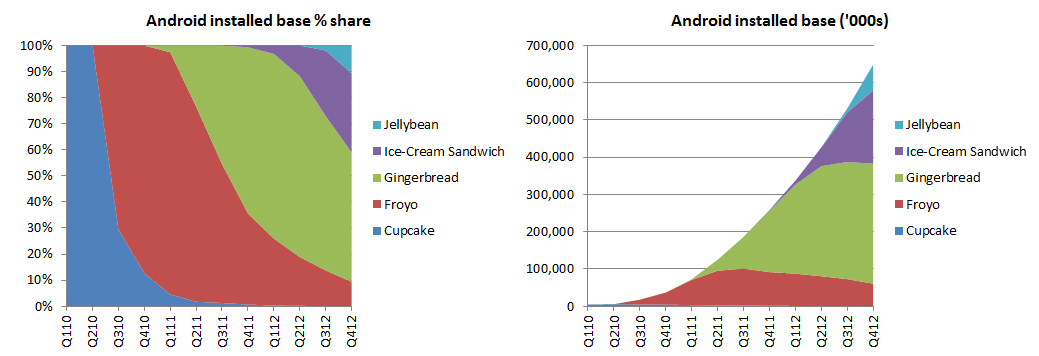

When I think back to where the Android store was at this stage in its cycle (say, 2010 when it was filled with plant-growing games and lots of random Russian porn apps), WP8’s offering is in much ruder health (albeit in a much competitive market). Back in the day the app selection on Android was really, really horrendous, but fast forward to present and it’s just not an issue. Soon I don’t think it will be an issue with Windows Phone either.

App ecosystem: The 95/5 rule

Another point is that even if you have 50+ miscellaneous games loaded up on your iPhone the reality is that 95% of the time you won’t be using them. For me what are the killer apps? A browser, a music app, a couple of social media feeds and a random killing-time-on-the-subway game. If I have these covered that’s 95% of my use-cases. I think most users are similar – and if that’s your hurdle then Windows Phone is more than enough.In terms of games particularly the 80/20 (or 95/5 rule) is definitely at work here. How many of us have bought a flashy Gameloft 3D shooter, installed it and realised three months later we never actually played the damn thing (too slow to load, no time to play). Although I see a lot of uber-premium driving or 3D shooters on the front page of the iOS App Store, I rarely see them being used on the tube. Instead it’s wall-to-wall Angry Birds.

The reason is that the dominant model on mobile is freemium which is based on getting a simple app which hits as wide an audience as possible and then relying on 1-2% of that vast base to get addicted and pay for top-ups. That is a model where a) iOS’s hardware advantages are less relevant and b) developers are incentivised to get their apps onto as many devices as possible – including WP8. Now it’s not there yet (Temple Run 2 would be nice), but if the dev-tools really are as easy to use as Microsoft say there seems to be little reason we won’t see an increasing number of ports coming to Microsoft.

A landmark low-end device

The Lumia 520 is a top-notch device, which offers excellent hardware design and a rich and compelling software experience. Yes there are gaps – multitasking, memory (perhaps), but not, IMHO, the app store selection (I think this is probably the first Windows Phone review in history which has made that statement!!).

But the point is for a sticker price of £109 the phone doesn’t have to be great. It doesn’t even have to be good (although it is). It just needs to spank the wave of Galaxy ace/ Alcatel / crapware “landfill smartphones”. And that it does in style.

The Lumia 520 is a half-price hero.

What this means for the smartphone war

What does this device mean for the smartphone industry? Two points:

1) The next war will be fought at the low end

|

The real competition: Huawei's Ascend G10. Dual core, more

polycarbonate than a Lego convention and yours for £130.

Source: Eurodroid.

|

At the high-end we have the Apple vs. Samsung slug-fest we all know and love. This is now a war of attrition – as Apple’s slowing growth shows the high end is becoming saturated and devices like the Galaxy S IV (and likely the iPhone 5S) show that evolution, not revolution, is now the order of the day. Highly profitable but not especially growing.

The mid-market (phones with an unsubsidised price of £200-400) is where things get squeezed. With the increasing quality of low-end devices (the Lumia 520 spanks most £200 android handsets for quality) the bottom falls out of this market, and if Google continues its aggressive Nexus push that hits the upper-mid hard. The Nexus 4 is effectively a high-end phone at a mid-market price point – and that’s had an impact. It’s the first Nexus phone I regularly see people using on my commute into work.

But the low-end is where the action is. Not only the Lumia 520 but the Xiaomi phone in China (with its excellent MiHome launcher - the only manufacturer skin people voluntarily install on their devices). In the US Blu are bringing low-cost Chinese platforms to the developed markets. Over here in the UK Aussie vendor Kogan (which has an interesting pre-sell-it-first-then-design-it model) has launched a £130 big-screen device in the UK (dual-SIM, no less!).

What we are seeing is a Cambrian explosion of competition at the lower end of the market. Let’s be clear it’s not going to be pretty and the margins aren’t going to be great, at least until competition dies down. But to me this is where the action is. This is something the commetariat seems to have largely missed; while endless ink has been spilt about why you should (or shouldn’t) get the GIV, I can count the number of Lumia 520 reviews on the fingers of my hand.

It will be interesting to see where the low-end Apple phone fits into this. Of course Apple’s “low-end” is everybody else’s “upper-mid”, so don’t expect too much. The question is whether their new device will reinvigorate the squeezed middle, or be swallowed by it. Their challenge is the (true) <£150 low-end is a market where Apple (which pays the bills with hardware gross) simply cannot go (as opposed to Nokia, which is desperate, or Google/Amazon, who don’t make money on hardware).

|

| Early traction in the Indian market. |

You can see this in the early traction in the Indian market, which has taken significant share out of the gate (see chart to right). Now success in a low-ASP market like India isn’t going to save their bacon, but a full quarter of 520 availability is undoubted going to give a boost to their Q2 Lumia numbers.

2) The market underestimates how competitive Windows Phone has become

It’s interesting if you look at broker forecasts for Windows. Despite the rapid rise of WP8 from a zero base they universally show its share inexplicably flat-lining at current levels. The fundamental issue for analysts is if they can’t forecast it, they just hold it flat. Better to be slightly wrong than either completely right or completely wrong.Except I’m pretty sure that’s the last thing that’s going to happen. If there’s one thing we’ve learned from the smartphone market over the last five years it’s that it never stands still. In 36 months’ time Windows Phone will either be zero percent or twenty percent of the market.

At the moment my bet is on twenty percent. As I’ve said I think the OS is a lot credible, and a damn sight better app selection than Android was at this stage in its evolution (and market share). For Microsoft failure is not an option – as mobile devices become primary devices, the mobile OS will become your primary OS. This is an existential threat for Ballmer & co.

This is the next war, and it will be fought at the low end.

{kind=link}